Development is no easy task.

We took a giant leap for this community in April: we partnered with a local insurance program for migrants in the area. This involved creating a few difficult boundaries in the community. First, we would no longer provide rides out to the free clinic; nor would we be footing any medical bills at clinics or hospitals. Instead, we would continue to provide basic medicine here in our home, and then help to subsidize the new insurance program.

To give you an idea, it’s an amazing deal. Healthy adults and kids pay $3 per month; basic chronic cases pay $5. Pregnant women who join pay an entry, plus $6 per month–which allows them to birth at the local hospital with C-section accessibility & their children receive official Thai birth certificates that can allow their children to become partial citizens if they stay to 18. Nearly all visits to the hospital, including surgeries and deliveries and bloodwork and admittance, are all free to the M-Fund member.

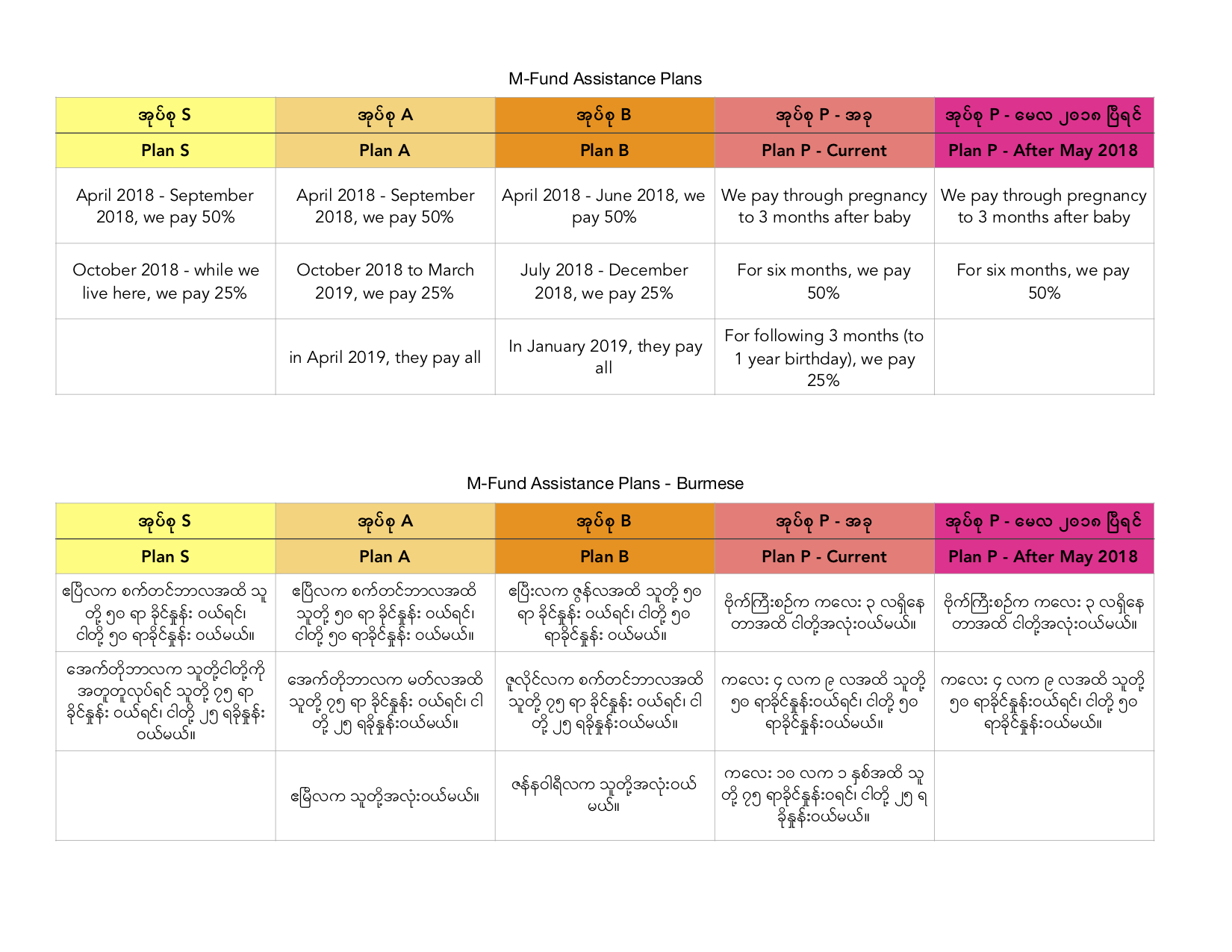

To help promote this in the community, we set up a subsidy system. It was a chaotic mess, involving colors and systems, and looked like this:

(If you’re really trying to understand the above mess, S = “staff” of The Breakfast Club, Flour & Flowers, The Reinforcers, Sojourn Studios, or our sewing project; A = you’re in our community and we know you well; B = you’re looking for a cheaper way to get insurance & we support that, but I wouldn’t know you in the market; P = pregnant.)

And yet, two months in, people were struggling to get their payments in on time. One month the payment fell on a Flour & Flowers delivery day, which found Thida and I sprawled on the floor with a pile of insurance numbers and names and money from the community and money from the House Fund and a couple calculators, all while the insurance staff waited for the money. I was late for deliveries. Thida had spent the whole day going door-to-door asking for premiums that people may or may not have. For about four families, Thida was paying for them and they’d “pay her back tomorrow.”

Something had to change, but it’s just always a challenge to maneuver. How do we encourage development: savings, investing in insurance, stability? But we also recognize and don’t want to belittle the real issues of poverty, struggling to make ends meet, being fearful of arrest, trying to get their kids fed, and trying to get clothes washed with water they are pulling out of a well. How do we inspire these families to value insurance enough to pay on time?

________________

In May, we had two families ask for money to pay for their kids’ school fees. We do value school, and we want to encourage kids to attend and parents to make that happen. But we also don’t feel it’s fair to have 90% of the families around us paying the fees, and yet we’re funding the last 10%. What will motivate them all to pay next year?

For each situation, we came up with a different solution. If there is one thing we have learned, every situation requires something different; something to fit this particular person or child, this particular financial situation, this particular need.

For the first situation, we really felt she didn’t have access to the money. Her husband was working and spending most of the money; it was a win if she & her son were given food in the scenario. Because of this, we were fairly certain we’d never see a single baht if we offered a loan. So we offered her an option to work off school fees. We’d pay the fees in full, and she had to work twenty days for The Breakfast Club, helping Thida. We also talked to Thida, explaining the opportunity for her to work off the school fees, as well as learn from a more experienced mother. We presented it to Thida as an opportunity: to talk to her about how to cook and serve healthy food; for how to discipline and set expectations for kids without hitting them.

Honestly, it’s been an epic success. She has since stayed on, hired to help Thida with breakfast every day. She’s eight months pregnant, and yet able to work a few hours in the morning to put money into her hands (very significant in some relationships), where she can make the choice for it to go to food or other necessities. She also has come to know and trust us; and has since spent a few nights at our house when she felt unsafe at hers. Her son comes for breakfast every day, and also gets to take some to school for lunch.

For the second situation, the husband did work and really did love his family. There are some budgeting choices that are difficult; but it’s clearly a choice to spend it on alcohol or save it for food, clothing, and school fees. For them, we offered a deal: we would pay the school fees in full, at $30. She would give back $3 per week: every week, on the same day, with no exceptions. If she was on time and had the full amount for 5 weeks–at which point she’d have paid $15, or half–that was all she had to pay. But for each payment she missed, she had to pay $3 more of the total.

Again (and surprise!)–an epic success. They didn’t miss a single payment. They were able to have school paid at half price, and we were able to have a successful loan system that didn’t weigh on our shoulders as we nagged and nagged for the next payment.

________________

With these two successes, we looked to M-Fund. How would we motivate this community to pay on time?

We couldn’t realistically offer everyone work to ensure they had the money, so we took Option #2! Last week we had yet another community meeting, to reiterate the value of M-Fund, to remind them that we will not always be here, and explain that this our effort to encourage a long-term improvement.

And we offered a simpler subsidy system. For anyone in with M-Fund in our community, money is due on the 29th of every month. If they submit their money by the 20th, House Fund will pay 50%. If they submit their money by the 25th, House Fund will pay 25%. And if they wait until the 29th, they pay the entire premium. We do have an exception for pregnancy: we begin at paying 100% on the 20th, if they ensure their entire group or family has paid by then.

Simply: If you value this enough to save and organize ahead of time, we’ll pay some. If you are disorganized or refuse to plan ahead, we won’t. And this will last until April, at which point it’s your responsibility to pay the full amount.

This did involve a re-working of the entire system, and if I’m honest, I’m tired of re-organizing health insurance programs in a Numbers chart, in Burmese.

But, we did have three community members go to the hospital this month for major issues: one for a CT scan (so expensive, but free!), one for surgery (so expensive, but free!), and another little toddler admitted with dengue (expensive enough, but free!). So I was motivated. Sure, let’s try this again!

As the 20th rolled around this month, just a week after our meeting to announce this, all but three members had their premiums paid in. Next week, we’ll be ready when the insurance staff As Thida and I went over the numbers and figures, she smiled, “Thank you so much. This is such a good idea. So much easier!”

So we’re just over here counting our wins.